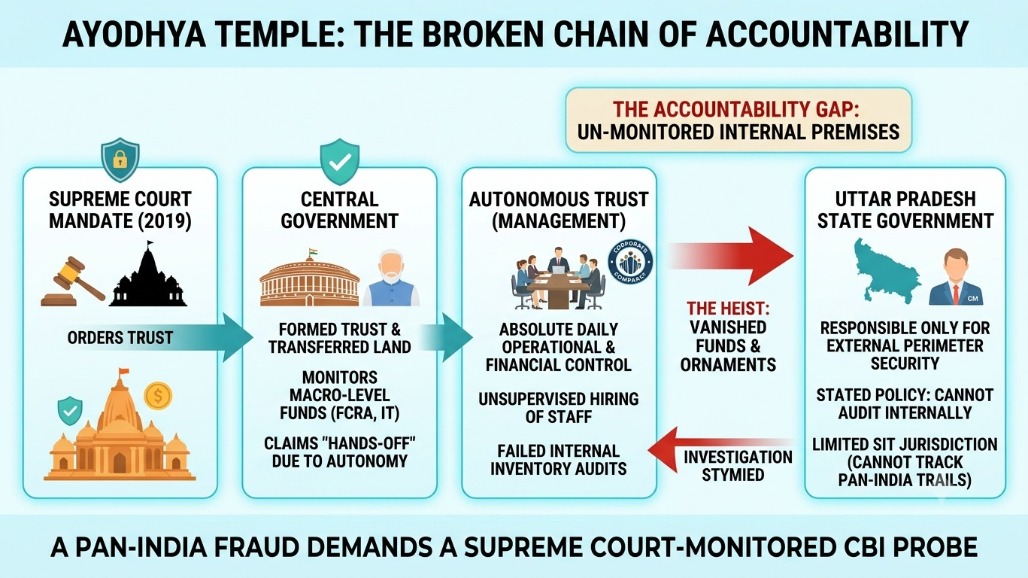

Why in news:

Recent allegations of irregularities in the handling of donations at the Ram Janmabhoomi Temple, Ayodhya, have reignited debate over temple governance in India. Amid concerns over financial management, the temple construction committee has suggested appointing a Chief Executive Officer (CEO) for better administrative oversight. Simultaneously, the Vishwa Hindu Parishad (VHP) has renewed its demand for reducing or eliminating state involvement in Hindu temple administration.

Scale and Nature of Temple Economy in India:

-

-

- India has an estimated 10 lakh Hindu temples, ranging from small village shrines to major pilgrimage centres. Large temples such as those in Ayodhya, Varanasi, Tirupati, and Haridwar manage substantial assets including land, gold, cash donations, and endowments.

- Donations often flow through charitable trusts, and registered entities may avail tax exemptions under Section 80G of the Income Tax Act, 1961. However, a significant portion of offerings—especially cash and in-kind donations—remains outside formal accounting systems, raising concerns about transparency.

- India has an estimated 10 lakh Hindu temples, ranging from small village shrines to major pilgrimage centres. Large temples such as those in Ayodhya, Varanasi, Tirupati, and Haridwar manage substantial assets including land, gold, cash donations, and endowments.

-

Traditional Systems of Temple Governance:

-

-

- Hereditary or Family-Based System: Many temples are managed by hereditary priestly families (pujaris or pandas). Offerings and ritual responsibilities traditionally remain within families, with administrative practices varying across regions.

- Mahant System: In this structure, a Mahant or spiritual head exercises complete control over temple administration, assets, and succession. Examples include several mathas and religious institutions founded under monastic traditions.

- Akhada (Panchayati) System: Akhadas are organised bodies of ascetics managing temples collectively. Leadership is usually elected or consensus-based, and they regulate rituals, resources, and institutional assets, particularly in Shaiva, Vaishnava, and Udaseen traditions.

- Hereditary or Family-Based System: Many temples are managed by hereditary priestly families (pujaris or pandas). Offerings and ritual responsibilities traditionally remain within families, with administrative practices varying across regions.

-

Role of the State in Temple Administration:

-

-

- State involvement in temple governance has historical roots in colonial laws such as the Religious Endowments Act, 1863, and the Madras Hindu Religious Endowments Act, 1925, which expanded regulatory oversight.

- Post-Independence, several states institutionalised temple management under statutory frameworks. Article 25(2) of the Constitution empowers the State to regulate secular and economic activities associated with religion, forming the constitutional basis for state control over temple administration.

- State involvement in temple governance has historical roots in colonial laws such as the Religious Endowments Act, 1863, and the Madras Hindu Religious Endowments Act, 1925, which expanded regulatory oversight.

-

Key Institutional Models:

-

-

- Tamil Nadu: HR&CE Department manages over 40,000 temples.

- Andhra Pradesh: Tirumala Tirupati Devasthanams (TTD) governed by a state-appointed board and CEO.

- Kerala: Travancore Devaswom Board oversees major temples including Sabarimala.

- Uttar Pradesh: Kashi Vishwanath Temple Board operates under government oversight.

- Tamil Nadu: HR&CE Department manages over 40,000 temples.

-

Issues in Temple Governance:

Key concerns include:

-

-

- Lack of uniform transparency in donation management.

- Weak auditing and accountability mechanisms.

- Political influence in appointment of trustees.

- Inequitable use of temple revenues.

- Tension between religious autonomy and state regulation.

- Lack of uniform transparency in donation management.

-

Way Forward:

Reforms may focus on:

-

-

- Mandatory digital accounting and real-time disclosure of donations.

- Independent financial audits of large temples.

- Professionalisation of temple administration.

- Clear separation of religious and administrative roles.

- Balanced legal framework ensuring both autonomy and accountability.

- Mandatory digital accounting and real-time disclosure of donations.

-

Conclusion:

The Ayodhya Trust controversy highlights a larger structural question in India: how to balance religious freedom, institutional autonomy, and public accountability in temple governance. A transparent and professionally managed framework, aligned with constitutional principles, is essential to maintain public trust while preserving the sanctity of religious institutions.