Why in News?

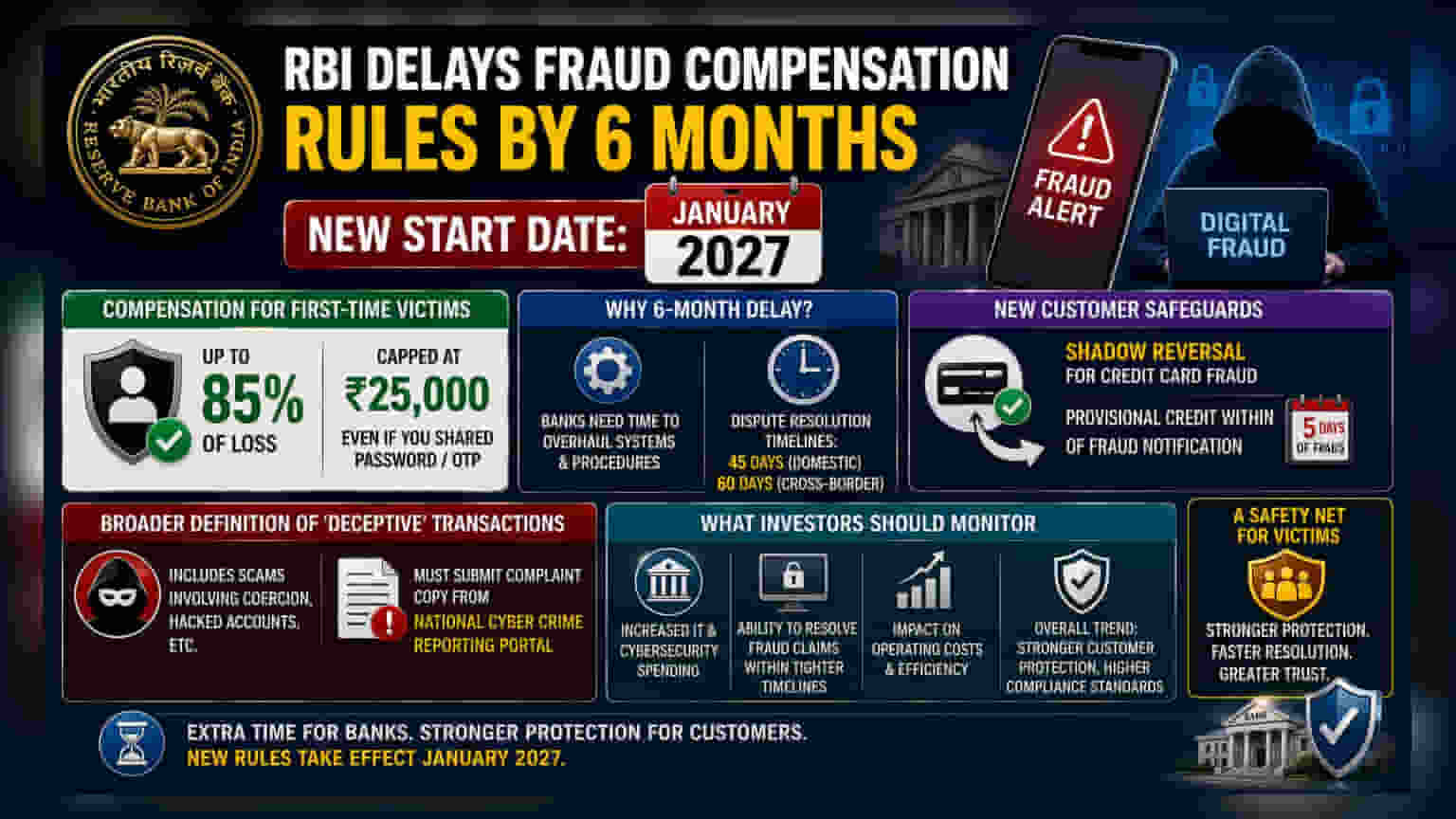

Recently, The Reserve Bank of India (RBI) has announced a revised compensation framework for victims of digital payment frauds under the RBI (Commercial Banks — Responsible Business Conduct) Third Amendment Directions, 2026. The new rules will come into effect for electronic banking transactions (EBTs) carried out on or after January 1, 2027. The move aims to strengthen customer protection as digital payment frauds continue to rise across the country.

Rising Digital Payment Frauds in India:

India's rapid adoption of digital payment platforms such as UPI, mobile banking, internet banking, and credit/debit cards has transformed financial transactions. However, it has also led to an increase in cyber frauds, including phishing, SIM swapping, OTP theft, fake UPI IDs, QR code scams, vishing, and AI-powered deepfake frauds. According to RBI data, the banking sector reported more than 36,000 fraud cases involving ₹13,930 crore during 2023–24.

Key Features of the New Compensation Rules:

-

-

- Under the revised compensation framework, a genuine customer who reports the fraud to both the National Cyber Crime Reporting Portal or Helpline 1930 and their bank within five calendar days will be eligible for compensation. This benefit can be claimed only once in a lifetime.

- For fraud losses of up to ₹50,000, victims will receive 85% of the net loss or ₹25,000, whichever is lower. The compensation will be shared between the RBI, the customer's bank, and the beneficiary bank in domestic fraud cases. In cross-border frauds, the RBI and the customer's bank will bear the compensation, as foreign beneficiary banks are excluded from liability.

- The revised rules also introduce special protection for credit card users. Banks must provide a shadow reversal, a temporary credit restoring the disputed amount, within five days of receiving a complaint. If the stolen money is later recovered, banks must recalculate the customer's actual loss and adjust the compensation accordingly.

- The RBI has already implemented several measures to curb digital payment frauds, including mandatory two-factor authentication, real-time fraud monitoring systems, and stricter action against mule accounts used by fraudsters. However, challenges such as low public awareness, poor recovery rates, cross-border cybercrime, and rapidly evolving AI-based scams continue to pose significant risks.

- Under the revised compensation framework, a genuine customer who reports the fraud to both the National Cyber Crime Reporting Portal or Helpline 1930 and their bank within five calendar days will be eligible for compensation. This benefit can be claimed only once in a lifetime.

-

Conclusion:

The RBI's revised compensation framework marks an important step toward building greater trust in India's digital payment ecosystem. By providing faster financial relief, clearly defining institutional responsibility, and strengthening consumer rights, the new rules seek to reduce the financial impact of online banking frauds.