Date: 26/11/2022

Relevance: GS-3: Basics of economics; Indian Economy and issues relating to planning, mobilization, of resources, growth,

Key Phrases: Cash in Indian Economy, Demonetization, Impact of Demonetisation, Monetary policy, Income Elasticity of currency demand, Velocity of money, Cashless Economy.

Context:

-

The cash intensity in the Indian economy has persisted despite policy efforts in recent times to promote less cash use through digitisation, formalization through GST and demonetisation of high currency notes.

-

The cash usages patterns have been out of sync with RBI estimates which has affected RBI’s liquidity management function.

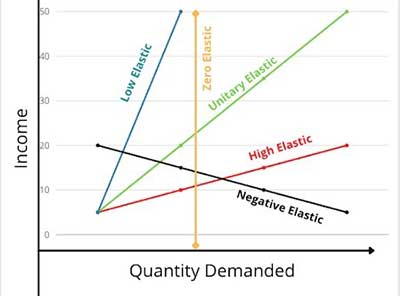

Income Elasticity of demand

- Income elasticity of demand is an economic measure of how responsive the quantity demanded for a good or service is to a change in income.

- The formula for calculating income elasticity of demand is the percentage change in quantity demanded divided by the percentage change in income.

- Businesses use the measure to help predict the impact of a business cycle on sales.

- Types of Income Elasticity of Demand

- High: A rise in income comes with bigger increases in the quantity demanded.

- Unitary: The rise in income is proportionate to the increase in the quantity demanded.

- Low: A jump in income is less than proportionate to the increase in the quantity demanded.

- Zero: The quantity bought/demanded is the same even if income changes

- Negative: An increase in income comes with a decrease in the quantity demanded.

- Income elasticity of currency demand:

- It indicates how the demand of currency in the economy is changing as the income of people change.

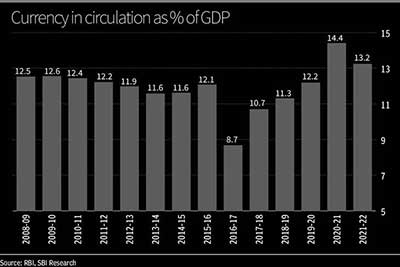

Currency demand scenario in Indian Economy

- High pace of expansion of currency with public (CwP)

- The pace of expansion of currency with public (CwP) has been above the trend since the mid-2000s.

- The pace even accelerated to record levels during the last four years ending FY2022 despite moderate nominal GDP growth and exponentially growing digital payments.

- SBI’s latest November Ecowrap shows an increase in currency in circulation (CwP plus cash held by banks) as a percentage of GDP post-demonetisation.

- The incremental currency growth during these four years even surpassed the CwP stock at end-March 2014.

- Income elasticity of currency demand is closer to unity

- Income elasticity of currency demand is closer to unity across the RBI’s currency demand models.

- It is expected to decline with a surge in cashless online payments, digitisation of direct benefit transfers and demonetisation-led formalisation of high denomination notes (HDNs) via bank deposits and restrictions on cash transactions.

- Factors which prevented reduction in cash demand

- Under-invoiced and illicit Chinese imports.

- Higher cash holdback by businesses due to systemic disruptions in trade credit flows (TC)

- These are among the many factors which neutralize the measures which could have reduced the demand for cash.

- Steady decline in decadal average income velocity

- Rising cash intensity is reflected in a steady decline in decadal average income velocity of CwP and M3 (broad money) over the last two decades.

- GDP/CwP and GDP/M 3 ratios declined from 11.26 and 2.15 in 1990s, respectively, to 9.37 and 1.25 respectively during FY 2011-22.

- These ratios touched a record low in FY 2021.

- Cash holding by public is significantly high

- Higher CwP/demand deposit (DD) ratio during FY2011-22 compared to 2000s shows rising cash holding by the public.

- There is marginal improvement in these ratios during FY 2022 compared to FY 2021 as FY 2021 was an abnormal year when GDP declined.

- Although given the situation on the ground, it is unlikely, despite the growth in digital payments, that the demand for cash will fall as steeply as policymakers anticipate.

Impact of cash to finance under-invoiced or illicit portion of imports

- The abnormally high cash intensity is led by the need for cash to finance under-invoiced or illicit portions of imports.

- These imports mainly from China are at the front and rising steadily since the mid-2000s.

- Discrepancies have been found between trade data sourced from the two countries, with invoiced imports being less than exports to India from China in the latter’s books.

- This can be manifested by various supportive evidence such as reports of Directorate of Revenue Intelligence, 145th Parliamentary Standing Committee on Commerce Report (Impact of Chinese Goods on Indian Industry, 2018), Global Financial Integrity, Washington etc.

- Recently the customs authorities have issued notices to 32 importers in September for alleged tax evasion of ₹16,000 crore through under-invoicing from April 2019 to December 2020.

Impact of negative trade credit (TC) conditions

- The negative trade credit leads to higher liquidity holdback by firms and reduces TC flows and its average repayment speed.

- Lower TC velocity pushes-up cash-intensity which further pushes liquidity held back and velocity of money drops.

- The TC crisis has been triggered by a string of events starting

from demonetisation, followed by GST and Covid waves.

- These led to trust and confidence contagion in the TC ecosystem which spurred a strong preference for cash sales.

- During periods of volatility such as Covid-19, demonetisation etc led to change in repayment behaviour, risk perception, business trust and liquidity conditions dramatically.

- This impacted the ability to repay, the willingness to repay in many cases.

- These drive more liquidity-holdback and strong preference for cash sales.

Way forward: Take ground realities into policy consideration

- The failed aim of flushing out black money in the form of HDNs — ₹500 and ₹1,000 through demonetisation in FY2017 shows that cash circulation in India is a complex phenomenon.

- Large part of cash circulation is thinly spread across household,

trading-network and manufacturing units.

- Also, the Chinese imports pervade our non-food consumption basket, trade and manufacturing structure.

- It was difficult to identify such thinly spread black money even as almost all HDNs were deposited in banks’ KYC compliant accounts during demonetisation.

- Therefore a better strategy would have been to check and control such imports at their entry point at ports.

- This also calls for an introspection on policy decisions and the need to devise policies which take ground realities into consideration vis-a-vis banking on textbook knowledge to effectively transmit fiscal and monetary policy decisions.

Source: Business Line

Mains Question:

Q. Despite digitalization there has been a persistent pattern of cash preference and cash holding in Indian economy, Evaluate. (250 words).